Categories

Buying a home, Clarksville TN Real EstatePublished June 8, 2026

Think You Need 20% Down to Buy a Home in Clarksville? You Probably Don't.

One of the biggest myths in real estate is that you need a 20% down payment to buy a home.

In fact, this misconception keeps many would-be buyers stuck on the sidelines for years while home prices continue to rise.

If you've been waiting until you save tens of thousands of dollars before purchasing a home, the good news is that you may already be closer than you think.

Where Did the 20% Down Myth Come From?

A 20% down payment has never been required for most homebuyers.

The number became popular because putting 20% down allows buyers to avoid private mortgage insurance (PMI) on many conventional loans. While that can be a great goal, it is not a requirement for homeownership.

Today, there are several loan programs designed to help buyers purchase a home with much less money upfront.

FHA Loans: As Little as 3.5% Down

FHA loans remain one of the most popular options for first-time homebuyers.

Benefits include:

- Down payments as low as 3.5%

- More flexible credit requirements

- Competitive interest rates

- Ability to use gift funds for down payment assistance

For many Clarksville buyers, an FHA loan can make homeownership possible years sooner than waiting to save 20%.

VA Loans: Zero Down for Eligible Buyers

Living near Fort Campbell means we work with military families every day.

One of the best benefits available to eligible service members and veterans is the VA loan program.

VA loans offer:

- Zero down payment

- No private mortgage insurance

- Competitive interest rates

- Flexible qualification standards

Many military families are surprised to learn they can purchase a home with little or no money down while building equity instead of paying rent.

Tennessee Down Payment Assistance Programs

Many buyers don't realize there are programs designed to help with upfront homebuying costs.

Depending on your income, occupation, and qualifications, you may be eligible for assistance with:

- Down payments

- Closing costs

- Grants

- Forgivable loans

These programs change periodically, but they can significantly reduce the amount of cash needed to purchase a home.

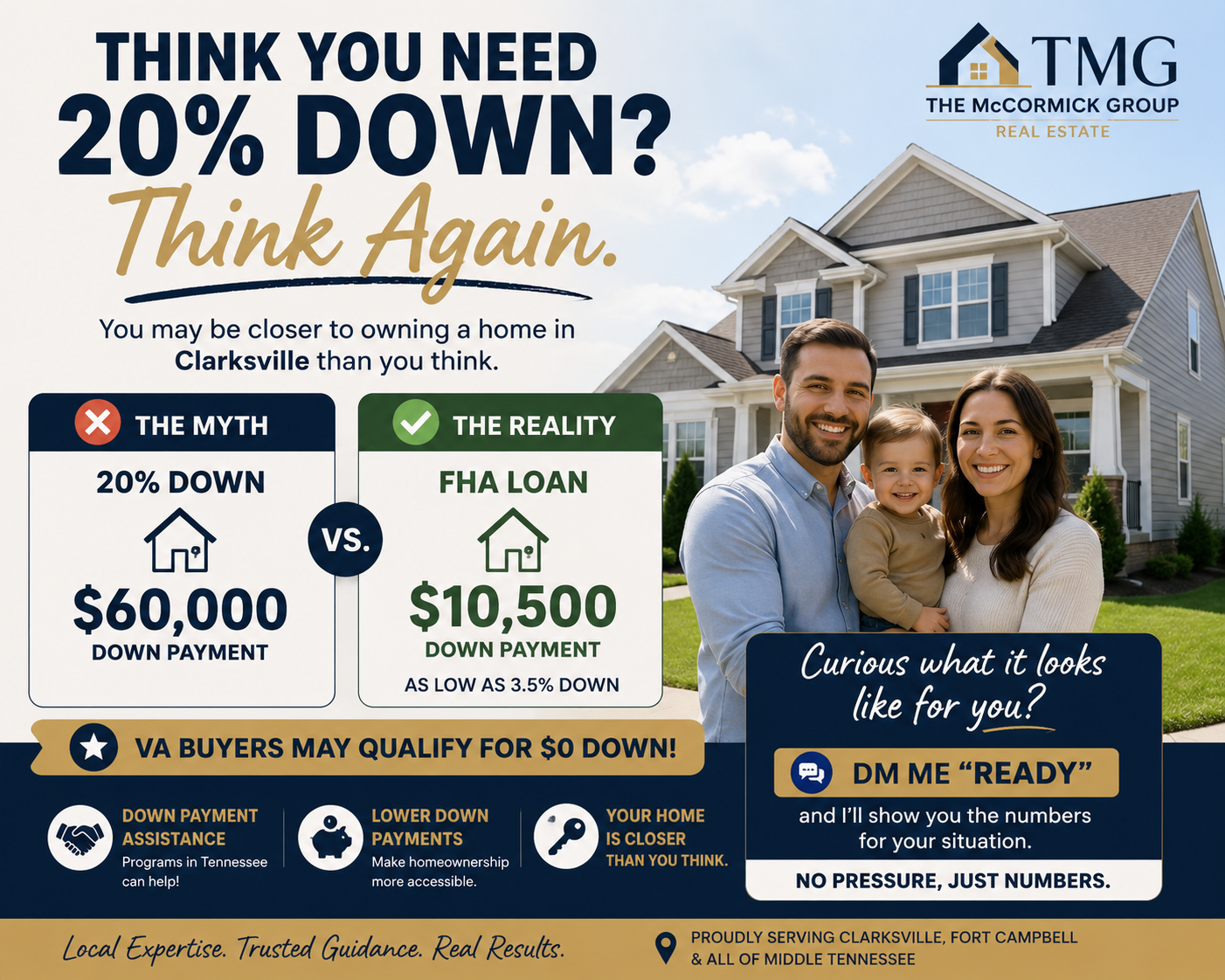

What Does This Look Like in Real Life?

Let's compare a $300,000 home:

20% Down Payment

- Purchase Price: $300,000

- Down Payment: $60,000

FHA Loan (3.5% Down)

- Purchase Price: $300,000

- Down Payment: $10,500

That's a difference of nearly $50,000.

For many buyers, the choice isn't between putting 20% down and 3.5% down.

It's between buying now or waiting years to save the larger amount.

Why Waiting Can Cost More

While saving for a larger down payment sounds responsible, waiting can sometimes be expensive.

During that time:

- Home prices may increase

- Interest rates may change

- Rent payments continue

- Opportunities to build equity are delayed

Every situation is different, which is why it's important to understand your actual options before deciding to wait.

How Much Do You Really Need?

The answer depends on:

- Your credit score

- Income

- Debt-to-income ratio

- Loan program

- Purchase price

- Eligibility for assistance programs

The only way to know for sure is to look at your specific situation.

Ready to See Your Numbers?

If you're thinking about buying a home in Clarksville, Fort Campbell, or anywhere in Middle Tennessee, I'd be happy to help you understand your options.

I'll show you:

- How much home you may qualify for

- Estimated monthly payments

- Available loan programs

- Potential down payment assistance opportunities

No pressure. No obligation. Just real numbers.

Contact Angie McCormick with The McCormick Group Real Estate for a free homebuyer consultation and personalized purchase plan.

|

or another way